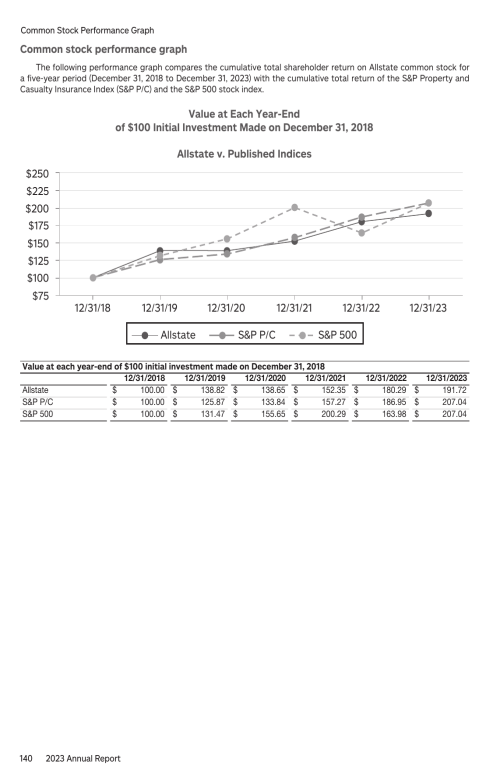

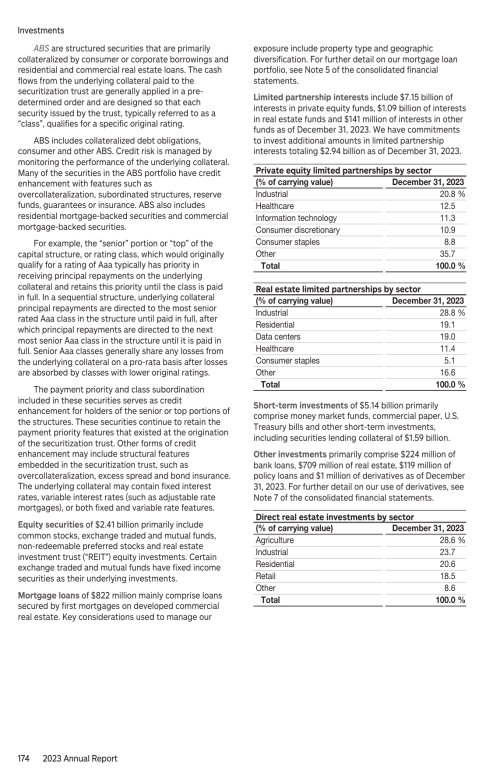

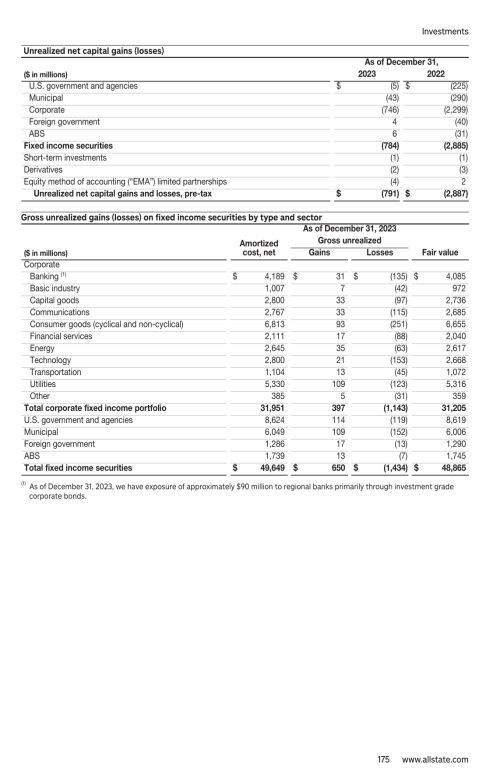

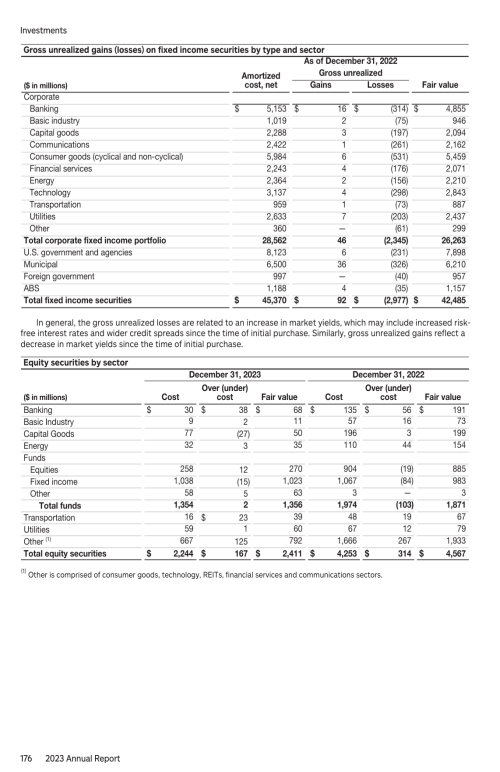

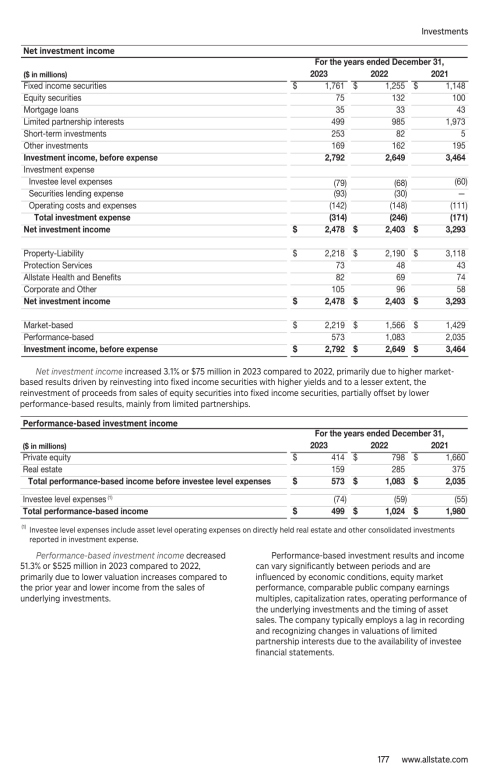

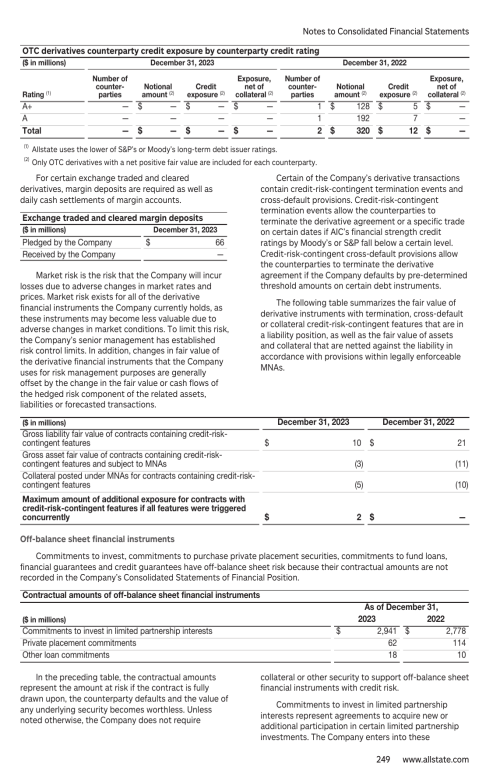

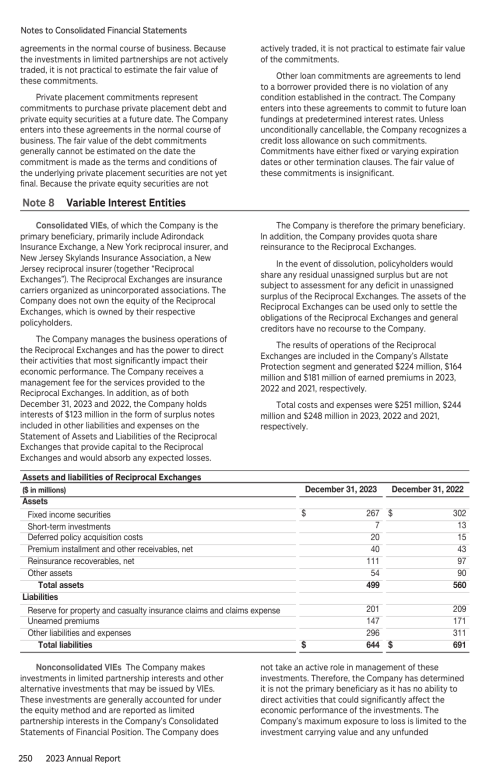

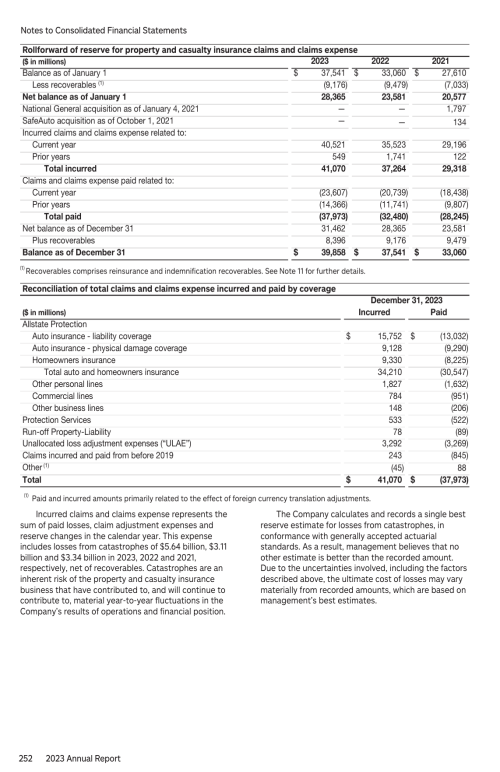

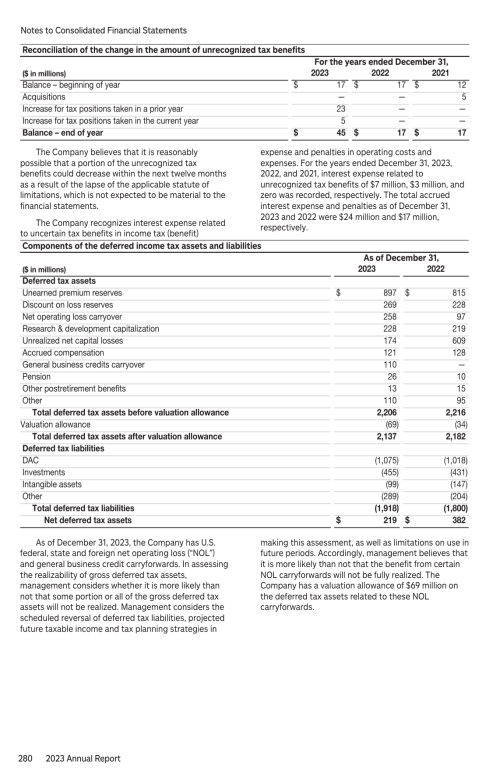

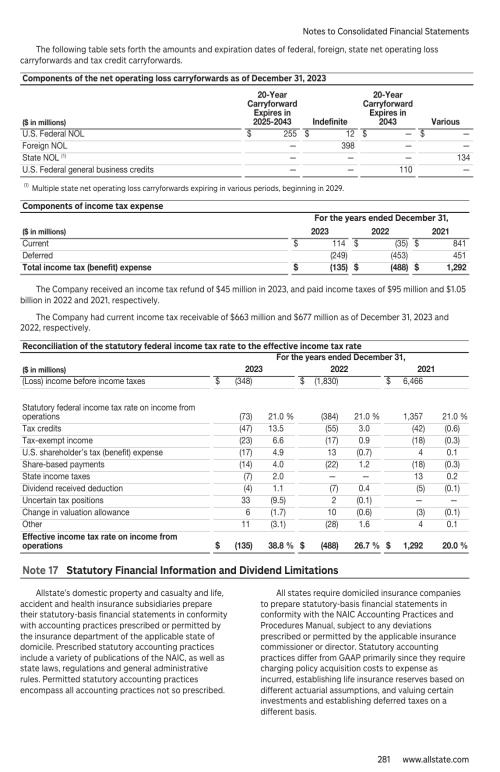

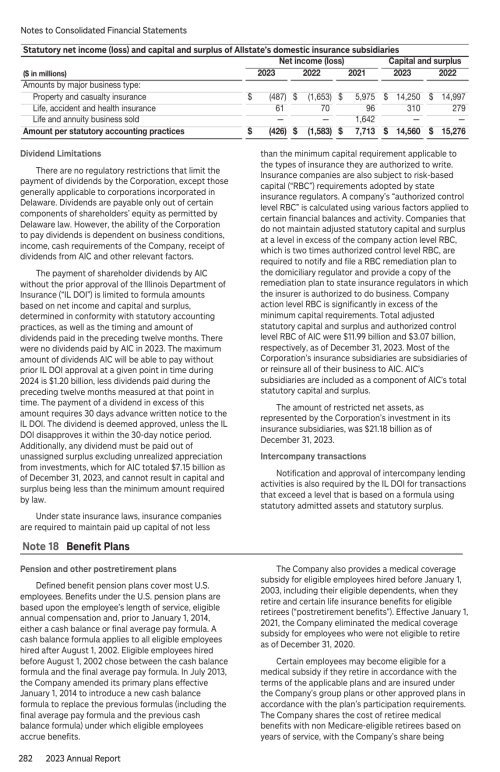

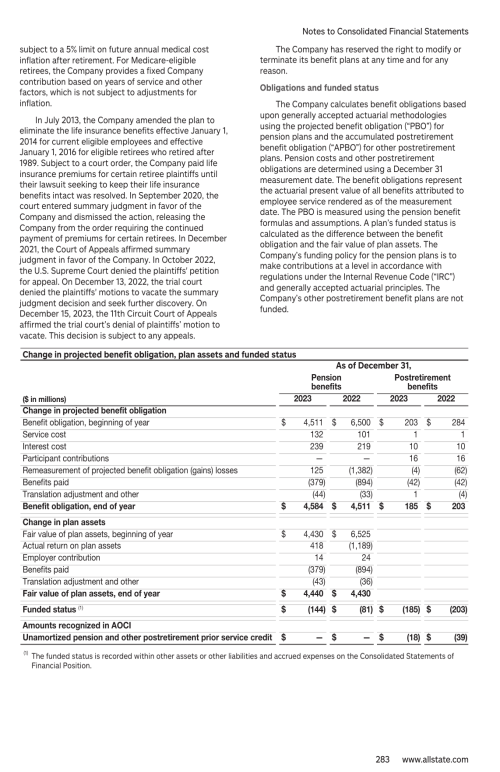

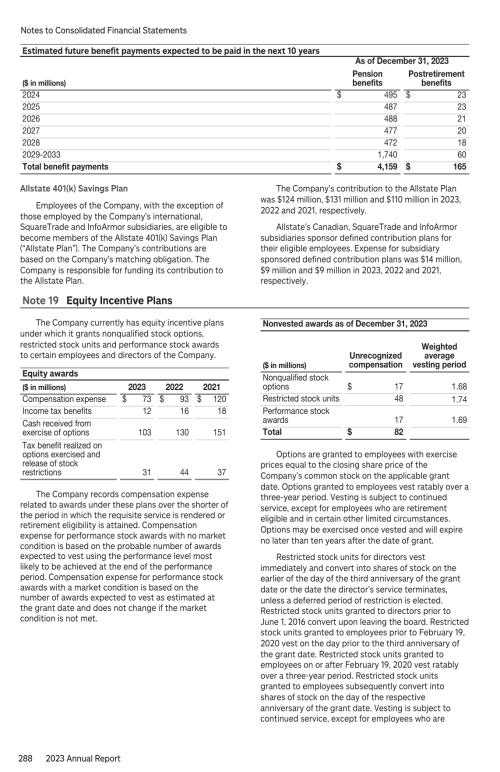

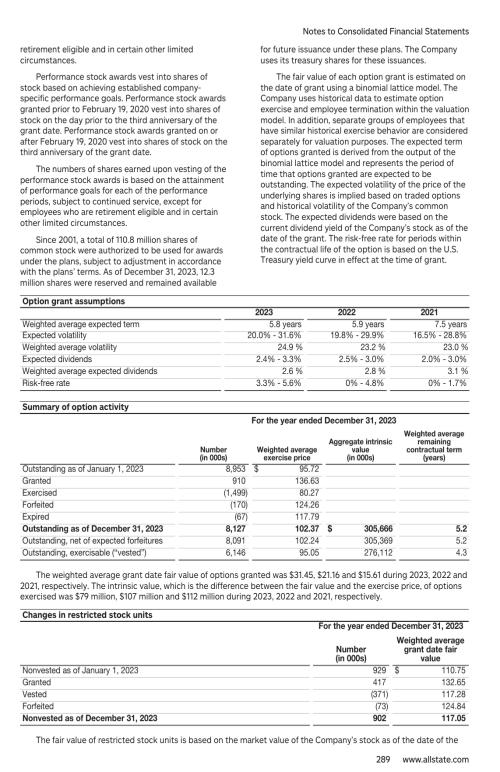

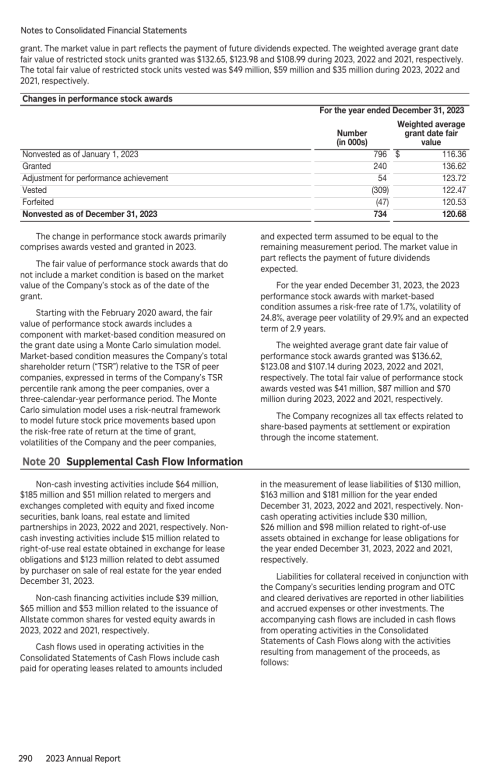

The Board recommends a vote FOR each director nominee

All candidates are highly successful executives with relevant skills and expertise

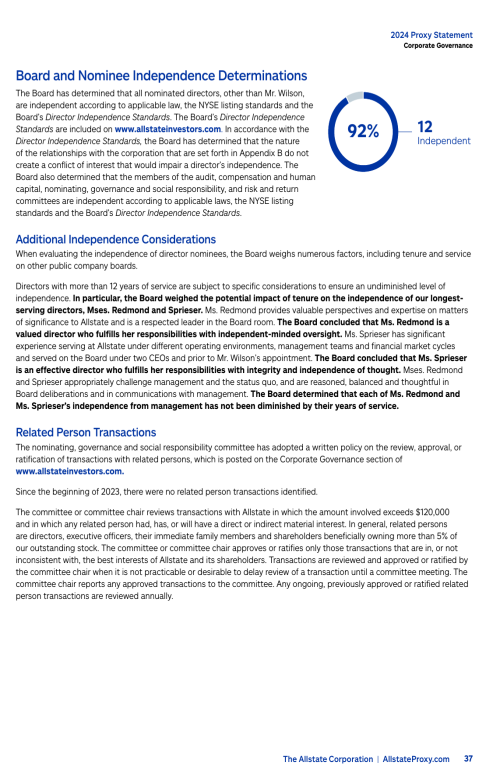

Average independent director tenure of 7.9 years, with 12 of 13 director candidates independent of management

Diverse slate of directors with broad leadership experience; 61% of the nominees bring gender or ethnic diversity, including three of the four committee chairs

Industry-leading shareholder engagement program and highly-rated corporate governance practices

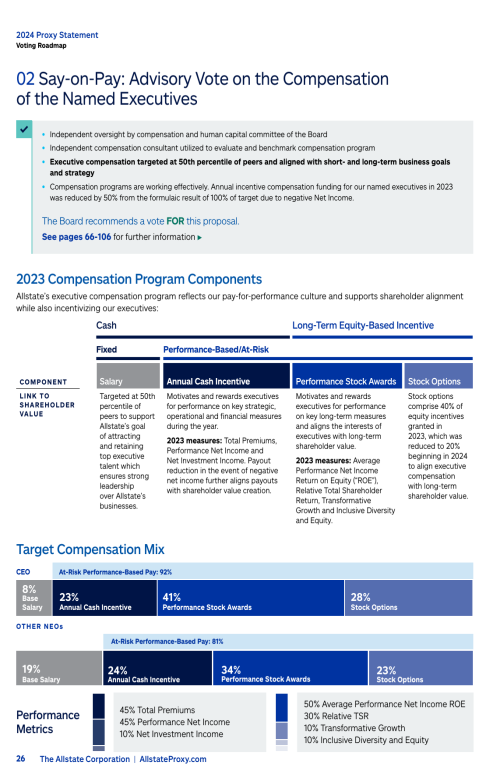

Proposal 2: Say-on-Pay: Advisory Vote on the Compensation of the Named Executives

The Board recommends a vote FOR this proposal

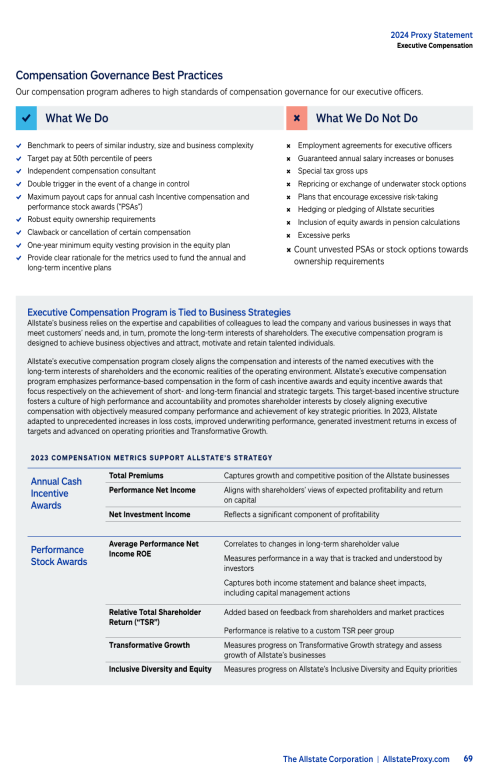

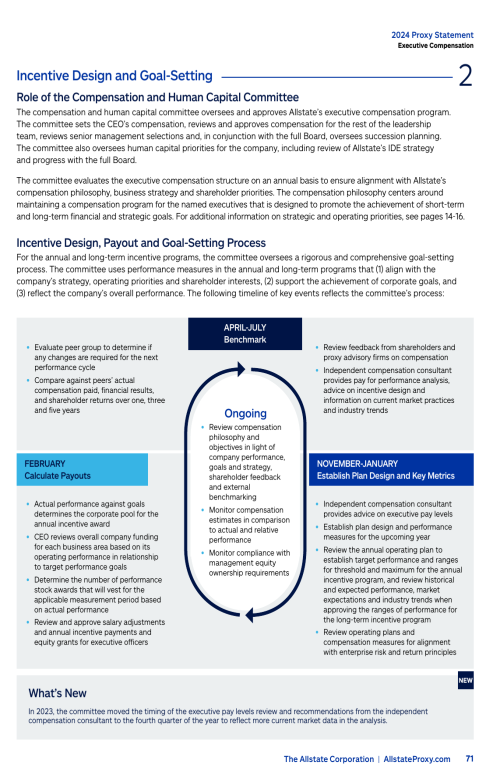

Independent oversight by compensation and human capital committee of the Board

Independent compensation consultant utilized to evaluate and benchmark compensation program

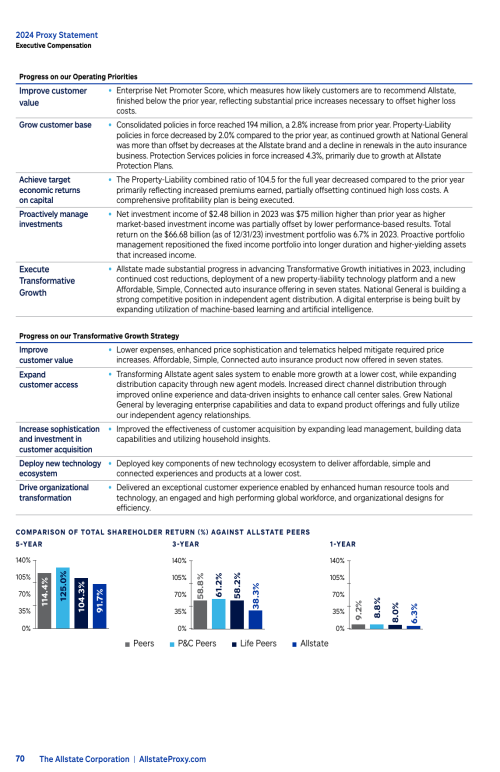

Executive compensation targeted at 50th percentile of peers and aligned with short-and long-term business goals and strategy

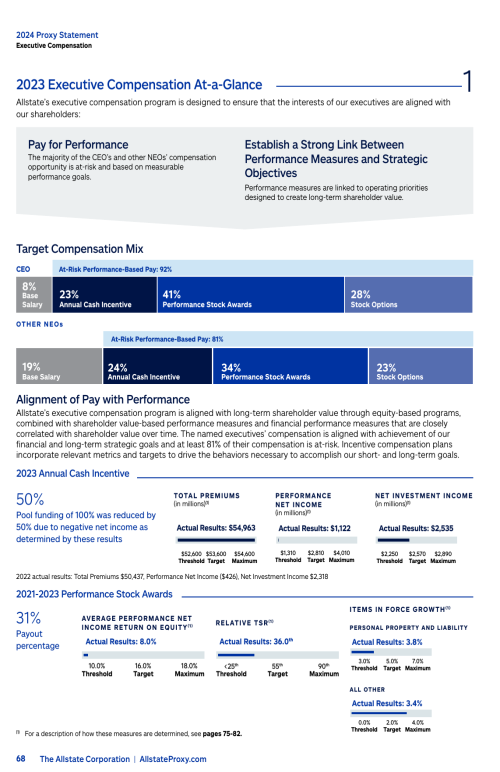

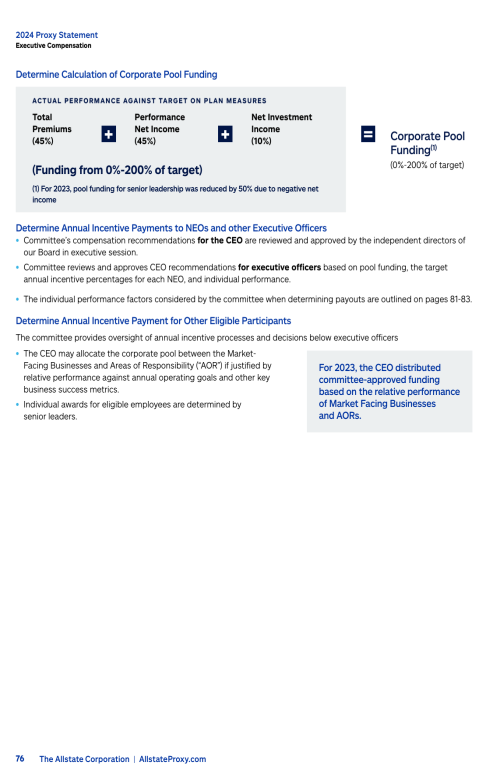

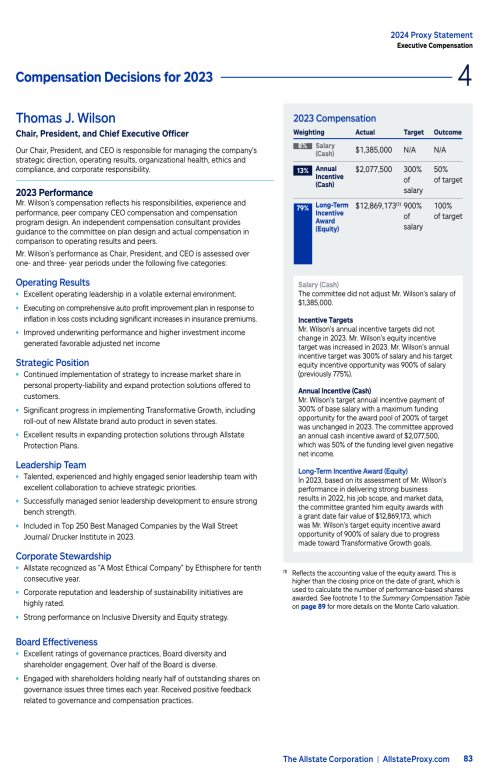

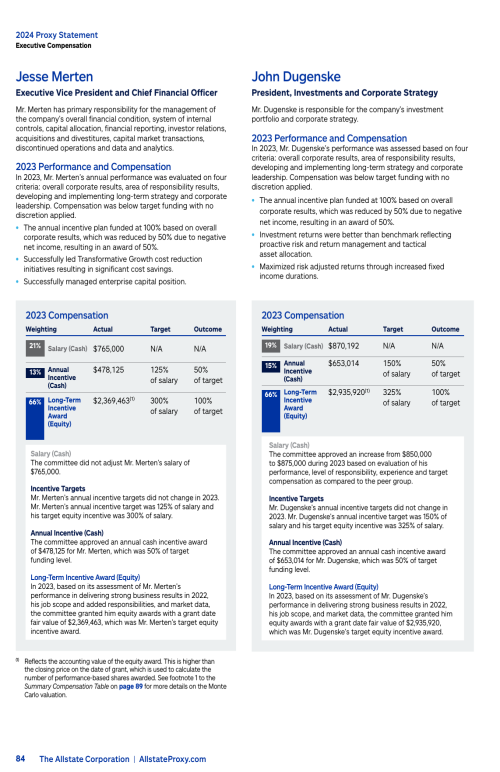

Compensation programs are working effectively. Annual incentive compensation funding for our named executives in 2023 was reduced by 50% from the formulaic result of 100% of target due to negative Net Income.

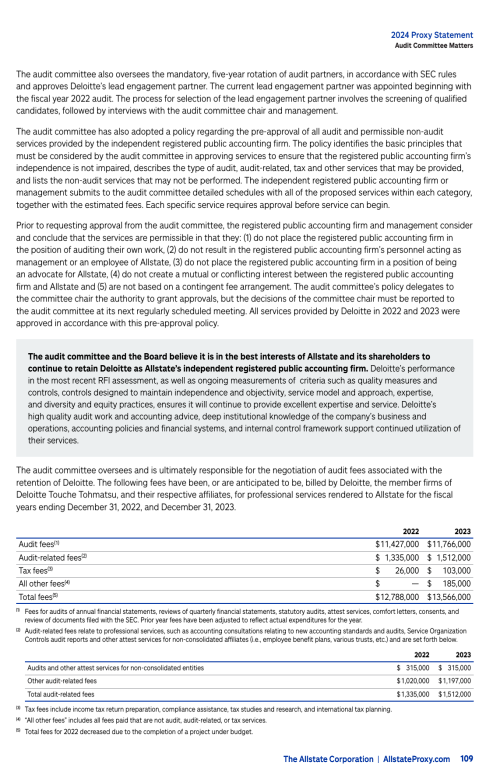

Proposal 3: Ratification of Deloitte & Touche LLP as the Independent Registered Public Accountant for 2024

The Board recommends a vote FOR this proposal

Independent firm with few ancillary services and reasonable fees

Significant industry and financial reporting expertise

The audit committee annually evaluates Deloitte & Touche LLP and determined that its retention continues to be in the best interests of Allstate and its shareholders